Energy demand is rising in China and world-wide at high speed. Oil and gas are getting scarce and expensive. Coal is available but causes big environmental problems locally and globally (global warming). Renewable sources of energy enjoy strong growth rates but will for a long time to come remain a limited option, chiefly for reasons of space and cost. Nuclear energy in relevant amounts will be facing serious problems of uranium scarcity (uranium prices rose much faster than oil prices in recent years), not to speak about the troubles with radioactive wastes, and the nuclear cycle’s vulnerability to terrorism and wars.

The core of the answer to the energy challenges may not come from modified energy supplies but from a systematic, long term strategy of increasing energy productivity, which essentially means curbing energy demand while further increasing prosperity.

As a matter of fact, huge efficiency increases are theoretically available. In a book, Factor Four, also available in Chinese [1], fifty examples were presented of a quadrupling of energy and material productivity. A more ambitious sequel, called Factor Five [2] is under preparation and will focus more on systemic productivity increases beyond isolated efficiency technologies. Eventually, even a factor of twenty should be feasible, which could solve most energy-related problems of climate, the local environment and social equity, both in China and world-wide.

A strategic increase of energy productivity looks like a highly attractive national goal for China.

Surprise lesson from history: resource prices have been falling

Despite basically well-known potentials, there are few signs in any country of aggressively pursuing the energy productivity agenda. Australia’s and other countries’ decisions of phasing out incandescent light bulbs, Japan’s top runner program, the EU’s emissions trading system ETS, and China’s commitment in the 11th Five Year Plan to increase energy productivity compare favourably with the inertia in other parts of the world. But even these laudable measures fall very far short of meeting the challenges.

The basic reason for inertia on this front, so it seems, is a world-wide policy of keeping energy prices as low as possible. This has understandable social reasons but it also sends a signal to consumers, manufacturers, and investors that energy efficiency and productivity will be mostly left to idealism or some mild state intervention. The trillions of yuans, dollars, and euros invested annually in new businesses and infrastructures have almost no commercial motive of addressing energy productivity. This is the reason why many of the of the Factor Four examples, such as Amory Lovins’ high tech ‘Hypercar’ needing less than 2 litres per 100 kilometres, have not made it to the market. For reaching the market in significant numbers, they require huge investments, which won’t pay off under present conditions.

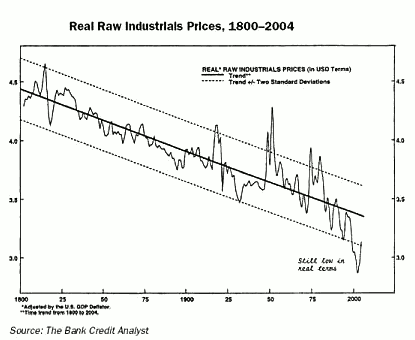

To make such strategic investments in resource productivity profitable, resource prices should go up. But so far, the opposite has happened. Combined efforts by politicians, entrepreneurs and mining engineers have established a long term trend of continuous decreases of resource prices, as shown in Fig 1 for “raw industrials”, meaning natural resources of industrial importance, including energy. This comes as a big surprise to many who are accustomed to complaining about high resource prices. The price hikes of the past couple of years have just brought us back into the lower confidence interval of the long-term downward trend. (The picture does not reflect the development after 2004!)

Fig. 1: Industrial raw resource prices, inflation adjusted over 200 years. Prospecting, mining and transport technologies were the main drivers. The price hikes since 2000 have just brought us back into the lower confidence interval of the downward trend! Source: The Bank Credit Analyst, 2005

There have been a few periods during which resource prices increased, notably the two World Wars. More memorable in our times have been the oil price shocks of the 1970s, which can also be seen in Fig. 1. In 1973, the oil exporting countries managed to quadruple oil prices overnight and push it further up in 1978. However, the rest of the world reacted by stepping up prospecting and mining until, by 1982, oil prices had come down to pre-1973 levels.

During the first years of the 21st century, many people felt that now, finally, resource prices were now going up irrevocably. The new surge of oil, gas and other mineral resource prices was triggered by steeply rising demand from the rapidly developing Asian economies, led by China. But China and the world wide mining companies have immediately thrown a lot of money into new prospecting and mining, which brought the surge to a halt and there are indications that commodity prices come down again, at least in constant dollars.

Typically, it is the geological limits and extraction and refinery cost that ultimately determine prices. In earlier decades, also access and transport limitations played a major role, but the share of transport cost has been falling systematically over time. If the geological limits remain the main determinant factor for resource prices, it can be assumed that oil prices will come down to something like $80 per barrel, reflecting the price of coal (at a high estimate of $100 per short ton of coal) plus the liquefaction cost at industrial scale plus company profits. Clearly, this price would be a blow to all investors putting their money into high tech vehicles like the Hypercar.

Active policies of raising energy prices

If markets (plus socially motivated price subsidies) lead mostly to low prices and if low prices are seen as the main obstacle to the efficiency revolution, then it would seem evident that China and the world should go for a policy shift from keeping prices low to actively increasing them.

Different instruments are available to put price tags on energy or, for that matter, on carbon dioxide. Theoretically, prices can be fixed by the state, — although in the past this was mostly done to keep prices low. Fees and charges can be levied. The EU’s ETS, a cap and trade regime, serves to put a price tag on fossil fuels. Some states, notably in Europe, beginning in Scandinavia, have introduced energy taxes.

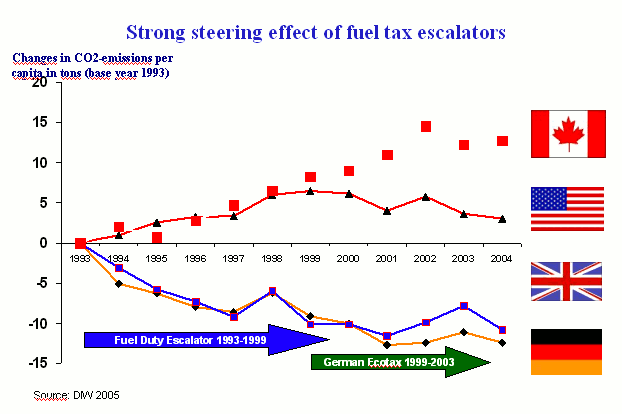

An interesting variant of energy taxation has been the “escalator” idea of adding small annual price signals that were agreed for many years in advance. This has been first introduced in Britain and copied in Germany with some modifications. In retrospect, it can be said that the escalator proved very effective in reducing demand, as can be seen in Fig 2, which compares the two countries with Canada and the USA with regard to fuel consumption/ CO2 emissions per capita and year.

Fig. 2: Steering effect of fuel tax escalators (Picture: FÖS, 2006, Database: DIW, 2005)

Increasing energy prices in parallel with energy productivity gains

Combining the escalator idea with the long term goal of increasing energy productivity, leads to a novel policy proposal, namely to politically establish a trajectory of steadily progressing energy and commodity prices, with the slope of the trajectory being determined by the statistically established increases of energy and resource productivity.

If energy prices increase only in line with average energy productivity gains, then, by definition, there would be no additional suffering. This is of highest political significance and contrasts favourably with experiences from the past of rising energy prices causing major hardship for families, small enterprises, and whole branches of industry. The negative effect, however, has always been associated with the size and suddenness of the price increase and with its unpredictability, allowing no advance adaptation.

Despite this socially most welcome feature, the long term escalator sends a strong signal to investors, manufacturers, consumers, and infrastructure planners to be prepared and to adapt. In all likelihood, the signal will actually accelerate investments into energy efficiency technologies and energy productivity creating systems.

The trajectory would have to be kept stable for many decades. Investors will be all the more courageous the longer they can rest assured of the trend. The time horizon of the measure should be at least as long as the payback time of the most important investments, meaning long lasting infrastructures. A glance back in history shows that under the conditions of the low gasoline prices in the USA, an investment like the Japanese bullet train (Shinkansen) would never have been possible.

Are there alternatives to a tax system for establishing the price corridor? Just theoretically, increasing resource prices can also be induced by an ambitious cap and trade regime with gradually tightened cap levels. However, past experiences with cap and trade regimes show very unpredictable fluctuations, resulting in part from speculation. There is no way of linking resulting prices to previous efficiency gains.

Is there a problem for the poor or industry or inflation?

Objections against an ecological tax escalator can come from advocates of the poor, from industry and from inflation fears.

Advocates of the poor will hint at the relative importance for the poor of the energy costs in the consumer basket. Energy and water taxes tend to be “regressive”, i.e. hitting the poor more than the rich. To answer this problem, it is possible to grant a tax free or tax reduced minimum tableau of, say, one gigajoule of energy per person and week. Then the really poor would actually benefit, while the burden would shift towards middle income and rich strata of the society.

Blue collar workers, too, have a tendency of opposing energy taxes. They typically use the lines of arguments of the poor and have apprehension that energy taxes might destroy industrial jobs. But as demand for industrial output is rising, a country like China need not fear net job losses if the price increase goes slowly and predictably.

Industry and investors are actually likely to benefit from the predictability of the transition. They can move into ambitious technological and infrastructural projects with very limited risks, leading eventually to major advantages over competitors working under conditions of fluctuating if somewhat lower resource prices who invariably giving too little attention to the long term scarcity of resources.

Another concern, very relevant in China today, is inflation. However, a tax shift could be made from value added taxes to energy, which a net neutral effect on inflation.

Evidently, it would be desirable for both ecological and economic reasons to find international agreement on price trajectories. But if the increase is linked to productivity gains, pioneering countries are likely to benefit, not loose because they will be at the forefront of a trend that will come world wide anyway.

The paradigm of a twenty-fold increase of labour productivity

The history of technological progress so far is the history of the increase of labour productivity. It has been a revolution indeed, the Industrial Revolution. Labour productivity grew easily twenty-fold over time. During the 19th century, the increase in what became to be the industrialised countries was some one percent per year, which is not all that spectacular. The rate increased to one and a half percent during the first half of the 20th century and to two percent thereafter. But there have been phases like Germany during the late 1950s, Japan during the 1960s and China after 2000, where it increased more than seven percent per year, — to a large extent by copying technologies that had been developed elsewhere.

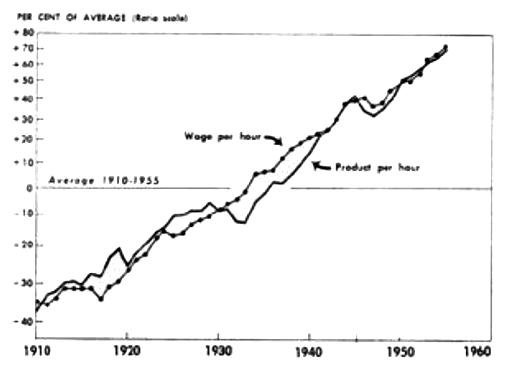

One fact, well-known by organised labour and by employers, is that wage negotiations have always taken labour productivity gains as their yardstick. It was only during the recent neo-liberal and neo-conservative phase since the early 1980s, that wages began to lag behind productivity gains, due mostly, as the employers saw it, to competition from low wage countries. What is not so well known is that productivity gains also went up in parallel with gross labour cost. What was the hen and what was the egg? Empirically, we observe wages and productivity going up in parallel (Fig 3).

Fig. 3: Rise of wages and of labour productivity mostly in parallel. The picture shows this for a time span of fifty years in the USA, but very similar pictures are available for other countries and other periods of time.

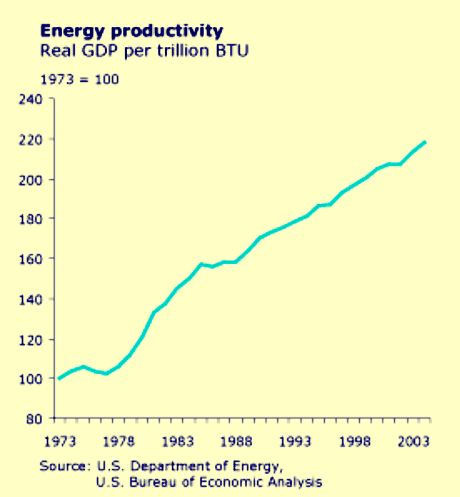

This trend of labour costs spurring labour productivity is an exciting indication for the potential of using energy price signals for spurring energy productivity gains. As a matter of fact, the “oil crisis” of the 1970s served as an (unplanned) experiment for this hypothesis. As energy prices went up across the board, a new mentality set in that focused on energy efficiency. Fig 4 shows the effect.

Fig. 4: The oil price shocks of 1973 and 1978 triggered a steady increase of energy productivity in the USA. The new mindset of energy efficiency survived even the period 1981–2000 of receding energy prices.

A revenue neutral ecological tax reform

The paradigm of labour productivity seems to support the idea of a steady increase of energy prices. As said before, if energy prices increase in line with average energy productivity gains, there would be no average suffering. The situation can become even more attractive if the fiscal income from energy taxes is re-channelled into the economy by reducing the fiscal or parafiscal load on human labour thus giving an additional push to overcome unemployment. But if inflation is the highest concern, the reduction of VAT is a more plausible candidate.

The new idea is to make the trajectory of energy prices very predictable by compensating world market fluctuations. Downward fluctuations would be compensated upwards and upward fluctuations such as the painful price hikes of late 2007 could be compensated downwards, so as to bring prices back to a previously agreed price corridor. The slope of the upward corridor could be determined annually (or every five years by the cycle of Five Year Plans) in line with measured average efficiency gains over the previous year (or years). Adjustments could be allowed on a quarterly basis so as to make prices even more predictable.

The system could be differentiated for vehicle fuels, electricity, carbon content, and other criteria. It will be a matter of political priority setting weighed against simplicity.

This system of increase should be made a law that is valid for some twenty years or even fifty or more years, with fairly tough clauses for exemptions or deviations from the rule.

It is conceivable to develop a similar system for materials and for water. If prices for primary raw materials and for water extracted from nature go up steadily, the incentives increase for reuse of materials and for water purification. Simultaneously, the profitability of mining operations go down, — which is exactly what we want.

Long term price elasticity is high

Generally, it can be said that energy and resource consumption have a rather low price elasticity in the short term. (Otherwise, the upward curve in Fig. 4 would have started in 1973 or 1974, not in 1977!) In the long run, however, the price elasticity is astonishingly high, as can be seen from an observation made by Jochen Jesinghaus [3].

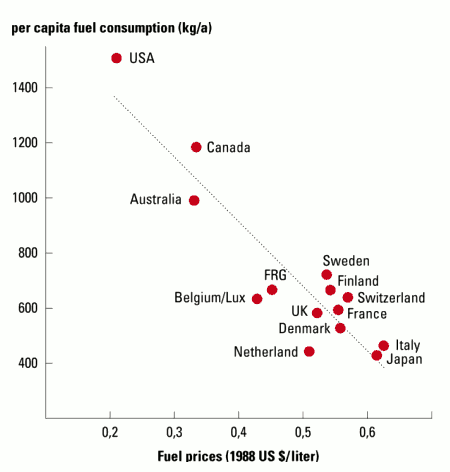

The picture shows a striking negative correlation between fuel prices and per capita fuel consumption. Ten years after the introduction in the US of the Corporate Average Fuel Economy (CAFE) standards, this country although admirably catching up on per mile fuel consumption was still the country with by far the highest per capita fuel consumption. In other words, under the condition of low fuel prices what CAFE conveyed to automobilists was: “Now you can drive more miles for your bucks”. Which they did.

Fig. 5: Even for petrol consumption which is often referred to as nearly inelastic to price changes, we observe a near perfect price elasticity – if we ask the right question. The question asked for this graph was: how much petrol is consumed per capita and year in different OECD countries that have nearly equal levels of wealth and mobility? Countries had more or less stable policies on domestic fuel prices for many years preceding the year (1988) in which the data were collected. The picture reflects long term price elasticity.

This experience is very valuable for determining a price trajectory overcoming the dilemma of short term instruments. We can safely rely on small signals if we give the society assurance of a long term upwards trend for energy and other resource prices.

[1] Von Weizsäcker, Ernst Ulrich, Amory Lovins, Hunter Lovins. Factor Four. Doubling Wealth, Halving Resource Use. London. Earthscan, 1997; also available in 12 other languages including Chinese.

[2] Von Weizsäcker, Ernst Ulrich, Charlie Hargroves, Michael Smith. Factor Five. London Earthscan, 2009.

[3] Ernst von Weizsäcker and Jochen Jesinghaus. 1992. Ecological Tax Reform. London, Zed Books.

CCICED Taskforce on Economic Instruments for Energy Efficiency and the Environment

Interim Report 2008, Draft segment submitted by Ernst Ulrich von Weizsäcker